Have you ever wanted something so badly, only to find out it’s nearly impossible to get? This feeling is at the heart of economics. It’s all about scarcity in economics: definition and importance.

We’re going to dive into what it means, why it matters, and how it shapes the world around us. Get ready to understand the fundamental problem that drives every economic decision!

Understanding Scarcity in Economics

Scarcity in economics is a core concept. It refers to the limited availability of resources in relation to unlimited human wants and needs. Simply put, we don’t have enough of everything to satisfy everyone.

This isn’t just about money. It’s about everything from time and clean air to raw materials like oil and gold.

The Basic Definition of Scarcity

Scarcity exists because our desires are endless. We always want more – more comfort, more entertainment, more resources.

However, the resources available to fulfill these desires are finite. This fundamental imbalance is what creates scarcity.

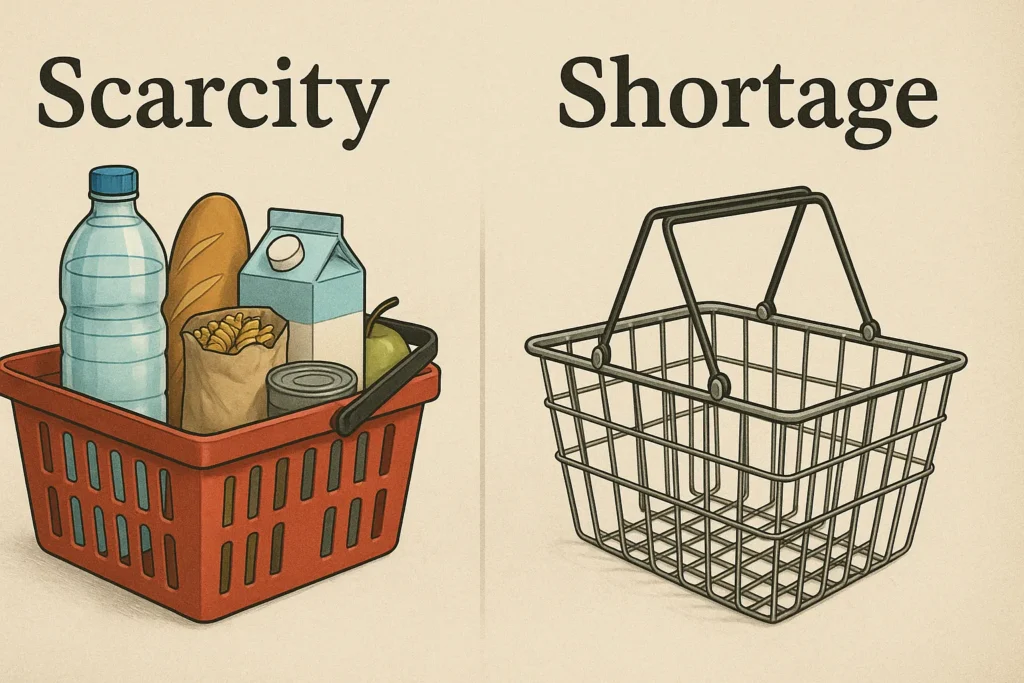

Scarcity vs Shortage: What’s the Difference?

It’s easy to confuse scarcity with a shortage, but they aren’t the same. A shortage is a temporary situation. It occurs when the demand for a specific good or service exceeds its supply at a particular price.

Scarcity, on the other hand, is a permanent condition. It exists because resources are inherently limited. Even if we could produce more of something, the resources used to make it would still be scarce.

Think of it this way: A shortage of gasoline after a hurricane is temporary. The scarcity of oil, however, is a constant reality.

The Role of Scarcity in Economic Decision-Making

Scarcity forces us to make choices. Because we can’t have everything we want, we must decide how to allocate our limited resources. This is where economics comes in.

Economics is the study of how societies manage scarce resources. It explores how individuals, businesses, and governments make decisions about production, distribution, and consumption.

Every decision we make involves trade-offs. Choosing to buy a new phone means giving up the opportunity to spend that money on something else. This is known as opportunity cost.

The Importance of Scarcity in Economics

Scarcity in economics is not just a theoretical concept. It has profound implications for how our economy works.

It influences everything from pricing and production to innovation and social policy.

Scarcity and the Price Mechanism

Scarcity directly affects prices. When something is scarce, its price tends to be higher. This is because people are willing to pay more to obtain a limited resource.

The price mechanism acts as a signal in the market. It tells producers what goods and services are in high demand. It also encourages consumers to conserve scarce resources.

For example, the high price of gold reflects its scarcity and the high demand for it. This incentivizes mining companies to explore for new gold deposits. It also encourages consumers to recycle gold jewelry.

Scarcity and Production Decisions

Scarcity forces businesses to make tough choices about what to produce. They must consider the availability of resources, the cost of production, and the potential demand for their products.

Businesses often seek to minimize their use of scarce resources. They aim to maximize efficiency and reduce waste. This can lead to innovation in production methods and the development of new technologies.

Scarcity and Innovation

Scarcity can be a powerful driver of innovation. When resources are limited, people are motivated to find new and better ways to use them.

This can lead to the development of new technologies, products, and services. It can also result in more efficient resource management practices.

For example, the scarcity of fossil fuels has spurred investment in renewable energy sources. This includes solar, wind, and geothermal power.

Scarcity and Government Policy

Governments play a crucial role in managing scarce resources. They can implement policies to promote conservation, encourage innovation, and ensure equitable distribution.

These policies can include taxes, subsidies, regulations, and public investments.

For example, governments may impose taxes on carbon emissions to discourage the use of fossil fuels. They may also provide subsidies for renewable energy projects.

Factors Contributing to Scarcity

Several factors can contribute to scarcity. Understanding these factors is crucial for developing effective strategies to address the problem.

Limited Natural Resources

The Earth’s natural resources are finite. This includes minerals, fossil fuels, water, and land. As the global population grows and consumption increases, these resources become increasingly scarce.

Overexploitation of natural resources can exacerbate scarcity. This can lead to environmental degradation and resource depletion.

Sustainable resource management is essential for mitigating the impact of scarcity.

Technological Limitations

Technology can help us overcome scarcity by increasing efficiency and productivity. However, technological limitations can also contribute to scarcity.

For example, if we lack the technology to efficiently extract a particular mineral, it may be considered scarce.

Investments in research and development are crucial for overcoming technological limitations. This can lead to new discoveries and innovations that expand the availability of resources.

Human Capital and Skills

Human capital refers to the skills, knowledge, and experience of the workforce. A shortage of skilled workers can limit a country’s ability to produce goods and services.

This can contribute to scarcity, especially in industries that require specialized expertise.

Investing in education and training is essential for building human capital. This can help to alleviate skill shortages and increase productivity.

Capital Goods and Infrastructure

Capital goods are the tools, equipment, and infrastructure used to produce goods and services. A lack of capital goods can limit a country’s productive capacity.

This can contribute to scarcity, especially in developing countries.

Investments in infrastructure, such as transportation networks and energy systems, are crucial for supporting economic growth and reducing scarcity.

Time Constraints

Time is a scarce resource for everyone. We only have 24 hours in a day, and we must allocate our time wisely.

Time constraints can limit our ability to produce goods and services, consume goods and services, and engage in leisure activities.

Effective time management is essential for maximizing our productivity and well-being.

Examples of Scarcity in Everyday Life

Scarcity in economics: definition and importance isn’t just an abstract concept. It’s something we experience every day.

Here are a few examples of how scarcity manifests in our daily lives:

Water Scarcity

In many parts of the world, access to clean water is a major challenge. Water scarcity can have devastating consequences for human health, agriculture, and the environment.

Factors contributing to water scarcity include climate change, population growth, and unsustainable water management practices.

Food Scarcity

Food scarcity is another pressing issue, particularly in developing countries. It can lead to malnutrition, hunger, and even famine.

Factors contributing to food scarcity include drought, conflict, and inadequate agricultural infrastructure.

Housing Scarcity

In many urban areas, housing is becoming increasingly scarce and expensive. This can make it difficult for people to find affordable places to live.

Factors contributing to housing scarcity include population growth, limited land availability, and restrictive zoning regulations.

Time Scarcity

As mentioned earlier, time is a scarce resource for everyone. We often feel like we don’t have enough time to do everything we want to do.

This can lead to stress, burnout, and a reduced quality of life.

Energy Scarcity

The world’s reliance on fossil fuels has led to energy scarcity and environmental concerns. As fossil fuels become depleted, the cost of energy is likely to increase.

This has spurred investment in renewable energy sources, such as solar, wind, and geothermal power.

Strategies for Addressing Scarcity

While scarcity is a fundamental economic problem, there are several strategies we can use to mitigate its impact.

Efficient Resource Allocation

Efficient resource allocation is crucial for maximizing the use of scarce resources. This involves making informed decisions about how to allocate resources to different uses.

Market mechanisms, such as prices, can help to allocate resources efficiently. However, government intervention may be necessary in cases where markets fail to allocate resources optimally.

Technological Innovation

Technological innovation can help us overcome scarcity by increasing efficiency and productivity. This can lead to the development of new technologies, products, and services that require fewer resources.

Investments in research and development are essential for fostering technological innovation.

Sustainable Consumption

Sustainable consumption involves using resources in a way that meets our current needs without compromising the ability of future generations to meet their own needs.

This can involve reducing waste, conserving energy, and using renewable resources.

International Cooperation

International cooperation is essential for addressing global scarcity issues, such as water scarcity and food scarcity.

This can involve sharing resources, providing technical assistance, and coordinating policies.

Population Management

Population growth can exacerbate scarcity by increasing the demand for resources. Implementing policies to manage population growth can help to alleviate pressure on scarce resources.

This can involve promoting family planning, improving access to education, and empowering women.

The Future of Scarcity

Scarcity in economics: definition and importance will continue to be a major challenge in the future. As the global population grows and consumption increases, the demand for resources will continue to rise.

Climate change is also expected to exacerbate scarcity by disrupting agricultural production and increasing the frequency of extreme weather events.

However, technological innovation and sustainable consumption practices offer hope for mitigating the impact of scarcity.

By investing in research and development, promoting sustainable consumption, and fostering international cooperation, we can create a more sustainable and prosperous future for all.

In summary, understanding scarcity is key to understanding economics. It shapes our choices, drives innovation, and influences government policy. Recognizing the factors that contribute to scarcity and implementing strategies to address it are essential for creating a sustainable future. What strategies do you think are most effective in addressing scarcity? Share your thoughts in the comments below!